What Are Revocable Trusts?

Although wills and trusts have no income threshold, nearly 50% of individuals who make over $80,000/year have a while compared to 24% who make less than $40,000.

And while COVID spurred many young people to create a will, the vast majority of Americans are still without protection.

If you have a will, you should consider adding a revocable living trust to accommodate possible changes in your future.

Defining Revocable Trusts

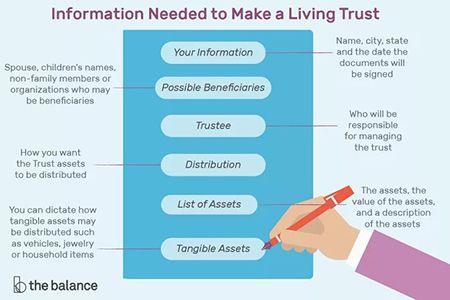

Revocable trusts are a collection of provisions and assets that the grantor can change.

Revocable trusts are living trusts, Inter Vivos Trusts, or loving trusts. Regardless of the name, the principle remains the same–it provides flexibility and income to the trustor (also known as grantor).

A living trust provides security because if the grantor experiences a health decline or dies unexpectantly, the assets in the trust can cover medical costs or go directly to the beneficiaries.

Although revocable trusts are excellent and offer many benefits, there are some things you should know about before creating one.

Pros and Cons of Revocable Trusts

Before creating a revocable living trust, you must be aware of a few pieces of information to help you make your decision. Here is a detailed list of the pros and cons of revocable trusts.

|

Pros |

Cons |

|

Flexible The grantor can change revocable trusts at any time during their life.

Income Since the assets in the trust are flexible, if you experience health problems or an emergency comes up, you can liquidate your assets for payment.

Termination The grantor can always end the trust if they deem it unnecessary.

Avoid Probate Court With most estate planning, assets and property must go to probate court before the beneficiaries receive anything. But in a revocable trust, everything skips probate court and goes directly to the beneficiaries. |

Upfront Costs Creating a revocable trust can cost thousands of dollars depending on the law firm, the state you live in, and the included assets.

No Tax Advantages Although some estate planning documents give you an estate tax break, a revocable living trust doesn’t. Since the assets are part of your estate, you must pay taxes on them.

Creditors Have Access Similar to the lack of tax advantage since you have a living trust, creditors can seize your assets if you fail to pay your debts. |

Establishing a revocable trust is a great way to prepare for the future but still leaves you with the flexibility to make changes throughout your lifetime.

However, the revocable trust doesn’t protect you from taxes or creditors during your lifetime or even after your death because the funds are available to cover costs accrued.

Is a Revocable Trust Right for You?

If you want to create a revocable trust fund, you need to speak with a law firm to help you start the process and fill out the necessary documents.

But before you fill out the paperwork, speak with the lawyers at Hickey and Hull Law Partners to determine if a revocable trust is suitable for you.